With a little dedication it is possible to minimize your debts individually. It is not constantly essential to discuss your situation with a debt therapist or register in some type of financial obligation combination program if you follow a couple of basic guidelines for financial obligation reduction.

Action 1: Evaluate your monetary circumstance

Collect all of your expenses, pay stubs and any other financial documents you have together with a current copy of your credit report. It is an excellent idea to examine your records against your credit report to make certain that you aren't attempting to pay back any financial obligations that aren't required or that have exceeded the applicable statute of limitations. Attempting to do so will restore these financial obligations! This is the primary step and frequently the most tough. You need to not only take note of the balances owed, but likewise the rate of interest, due date, annual fees and other qualities of the financial obligation that could affect your financial circumstance.

Action 2: Budget Plan Evaluation.

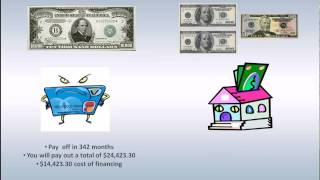

After you have actually recorded all of your financial obligations, have a look at your month-to-month expenditures and assess your budget plan. An excellent place to begin is identifying your "Take Home" Pay (Earnings after your taxes and withholdings). After you determine your Take Home Pay, you need to deduct the repaired costs that will remain the very same monthly and requirements for a living (i.e. mortgage/rent, vehicle expenditures, child care, trainee loans, insurance coverage, energies, groceries, etc). After you have computed all of this, what is left need to be used for repayment of debt and other discretionary costs items. If you are not able to support the financial obligation, your next step would be to identify a way to minimize your month-to-month living costs. Questions you should ask yourself are, can I decide for the lower telephone strategy, or lower my regular monthly cable bill? Sometimes we start to puzzle required costs with luxury expenditures. The more loan you can commit monthly to paying off your debt, the faster you will be living debt-free. When making the minimum payments, the overwhelming bulk of the cash paid is used specifically to cover the interest rates you are paying. This is the manner in which your banks/creditors earnings and http://www.thefreedictionary.com/https://www.mapquest.com/us/colorado/pinnacle-one-funding-422295107 you will find yourself on a "Debt Treadmill" so to speak, without any way to ever get off. Your financial obligation can frequently take lots of years to pay back. Please see the minimum payment calculator on our web page to calculate the length of time it will take to settle your debt if just making minimum payments. By making payments in excess of your minimum payments, you can in fact start to pay down the principal owed.

Step 3: Course of Action

Now that you have a more thorough understanding of your own financial circumstance, you ought to develop a strategy for reducing your financial obligation. If you subtract the minimum payments determined in step 1 above and the month-to-month expenditures calculated in step 2 above from your "Take Home" pay, you will have all staying discretionary loan available to you. Discretionary loan explains the cash that is available to you for all leisure products that aren't essential for living. Your objective should be to apply as much of the discretionary loan you have available towards settling your debt. You should start with the greatest interest rate cards/debts and work your method down. This will be the quickest way to settle your financial obligations. It is an excellent idea to prevent using your credit so that you do not contribute to the issue and discover yourself back to square one.

Step 4: Work out with your lenders

In these difficult financial times, much of your financial institutions will be understanding to your predicament. If you have a legitimate difficulty, they may be understanding of your circumstance and can potentially deal with you. It is a great concept to pick up the phone, describe your scenario, and simply ask the lenders if they can do anything to enhance the regards to your contract with them. Some potential support they might provide would be to lower your rate of interest and even negotiate a lowered balance on some of your financial obligations. You will have greater success negotiating the terms on debt that Pinnacle One Funding is already overdue or charged-off (dismissed by your lender and sold/turned over to collections). If you are receiving deals of credit, you need to think about moving balances to brand-new credit cards with a 0% introductory rate for 6-12 months or just merely a lower rate. If most of your payment is being used to the principal because your interest is so low, you will discover yourself minimizing your financial obligations much faster. Ensure to focus on the portion of your debt relative to your limit. Card balances above 35% of the limitation can even more damage your credit rating.

Step 5: Devotion

A plan is only as good as the dedication you make to keeping it. Getting out of financial obligation requires discipline and persistence. You did not enter financial obligation over night and you will not leave financial obligation overnight. You must be patient with the process and fulfill your payment objectives each and every month. If you follow these actions, you might put yourself in a position of financial security and stability.